Struggling with Financially Unstable Father-in-Law: What Should We Do?

Navigating financial support for a struggling father-in-law presents tough choices—should you prioritize your own goals or extend aid to family members in need?

It started with a simple ask, and it quickly turned into a full-blown budget standoff. OP’s wife told him her dad is behind on bills, drowning in private loan debt, and basically out of options, then looked at him like, “So… can we help?”

Here’s the messy part, they’re not rolling in extra cash. OP is working full-time, but they’re saving for a house and paying down debt. His wife works just 1 to 2 days a week right now, mostly because she’s the full-time babysitter for their 6-month-old, and in July she’ll go full-time once OP’s mother retires and takes over daycare.

Meanwhile, her dad is a month behind on the electric bill, needs about $400 for HVAC so the air actually works, and owes over $50,000 in private loans he took out in his own name to pay for his kids’ college, while both kids seem to be dodging the responsibility.

Original Post

My wife informed me this week that her dad isn't doing well financially. She asked if we could give him some money to help him, but we don't have a lot of money to be doling out.

We're currently saving up for a house of our own as well as paying down some debt. I work full-time, but my wife only works 1 to 2 days a week currently.

Her main job now is taking care of our 6-month-old. Come July, she'll be working full-time when my mother retires and takes over "daycare" duty during the week.

Here's what I've been told about her dad's situation: he's a month behind on his electric bill—roughly $250 to get him current.

He has to pay around $400 to have his HVAC system serviced so that the air conditioning will work properly for this summer. He owes over $50,000 in private loan debt that he can no longer keep up with due to the interest.

These private loans were apparently taken out in his (father-in-law's) name, and the money was used to put two of his children through college. I do not know why the children didn't get the loans themselves; regardless, one of them works part-time at Home Depot, and the other one is essentially unemployed.

Neither of them seems to be taking responsibility for this debt. The father-in-law doesn't have a regular job.

He works in a bar and DJs. I've been told he has no money saved for retirement—no insurance—nothing of the sort.

I'm not keen on trying to tackle any of this, but I also understand my wife's desire to help her dad. I'm not really sure how to approach this situation.

My gut tells me that my father-in-law needs to tell his two kids to start paying down that debt. Both of them still live with him, and I feel this is a "they need to pull their weight around the house" kind of conversation.

I'm just not really sure what to do here.

Financial obligations to family can create significant emotional stress.

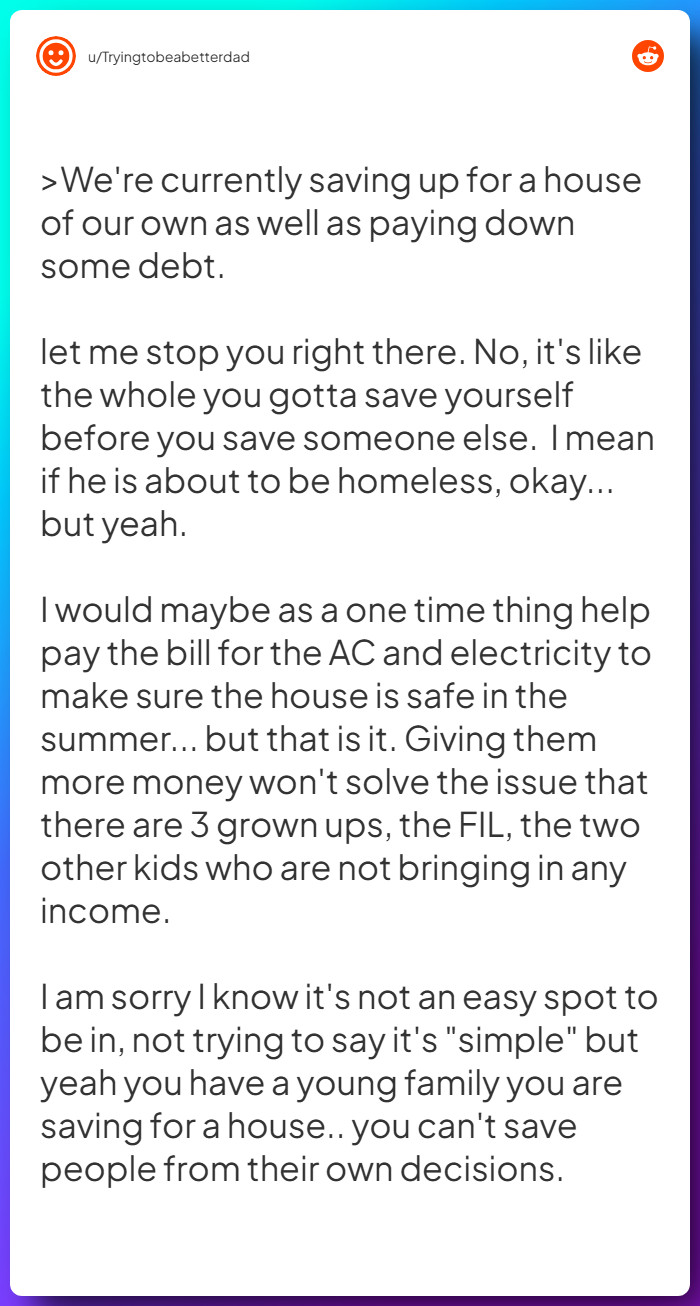

Comment from u/Tryingtobeabetterdad

Comment from u/brauxpas

Comment from u/bjlled

OP’s wife brings up the $250 electric catch-up, and suddenly “just a little help” sounds like a trap with a price tag attached.

Creating a family budget together, where everyone contributes ideas, can also promote accountability and shared responsibility. This collaborative approach can help the father-in-law manage his finances while encouraging the adult children to contribute to the household.

Comment from u/[deleted]

![Comment from u/[deleted]](https://static.postize.com/posts/comments/comment_68e79a86f41b8.jpg)

Comment from u/bridges-water

Comment from u/goinhuckin

When family members understand one’s limits, it encourages them to seek solutions independently rather than becoming overly reliant on others for financial support.

Comment from u/RespectTheTree

Comment from u/pigeonholepundit

Comment from u/RedditorFor1OYears

The HVAC bill hits next, around $400, and OP can practically feel summer turning into another emergency expense.

Also, if you’re stuck weighing responsibility and money, the diner battling “I’m Not Cheap, I Swear!” over tipping shows how messy it gets.

Consider utilizing resources such as workshops or online courses that focus on these aspects. By improving financial literacy, families can break the cycle of dependency and create a more sustainable financial future.

Comment from u/MultiPass21

Comment from u/ImportantPresence694

Comment from u/Boysenberry-Dull

Then the real bomb drops, more than $50,000 in private loan debt, tied to college money and a bar-and-DJ lifestyle with no job stability.

The emotional strain that financial instability exerts on family dynamics is evident in the scenario presented.

Comment from u/dfphd

Comment from u/Lucky-old-boy

Comment from u/kezinchara

Creating a plan for financial support can help alleviate the burden on one family member.

Comment from u/Viot

Comment from u/No-Pair788

Comment from u/[deleted]

![Comment from u/[deleted]](https://static.postize.com/posts/comments/comment_68e79aa05dd6d.jpg)

The two kids still living with him, one working part-time at Home Depot and the other basically not working, and OP’s gut says the conversation has to go there, fast.

Effective communication is crucial when navigating financial support within families. Many conflicts arise from misunderstandings about expectations and responsibilities.

These discussions can lead to clearer expectations and collaborative problem-solving. When everyone involved understands the situation fully, it can help mitigate feelings of guilt or resentment, creating a healthier family dynamic.

Comment from u/keyh

Comment from u/foolproofphilosophy

We'd love to hear your take on this situation. Share your thoughts below.

This situation highlights a common psychological conflict: the tension between familial obligation and personal financial security.

In navigating the complexities of financial instability within family dynamics, the situation presented in the Reddit post highlights the need for a careful approach that balances compassion with practicality. The emphasis on financial literacy and transparency is particularly relevant here, as understanding each other's financial situations can pave the way for collaborative solutions. By fostering a family culture that values both emotional support and financial responsibility, families can work towards healthier relationships and more sustainable outcomes for everyone involved.

The hard part isn’t the money, it’s whether the family will ever stop paying for everyone else.

Before you decide, read about the teen who endured a secret vape, toxic room, and toilet-dipped makeup wipe.