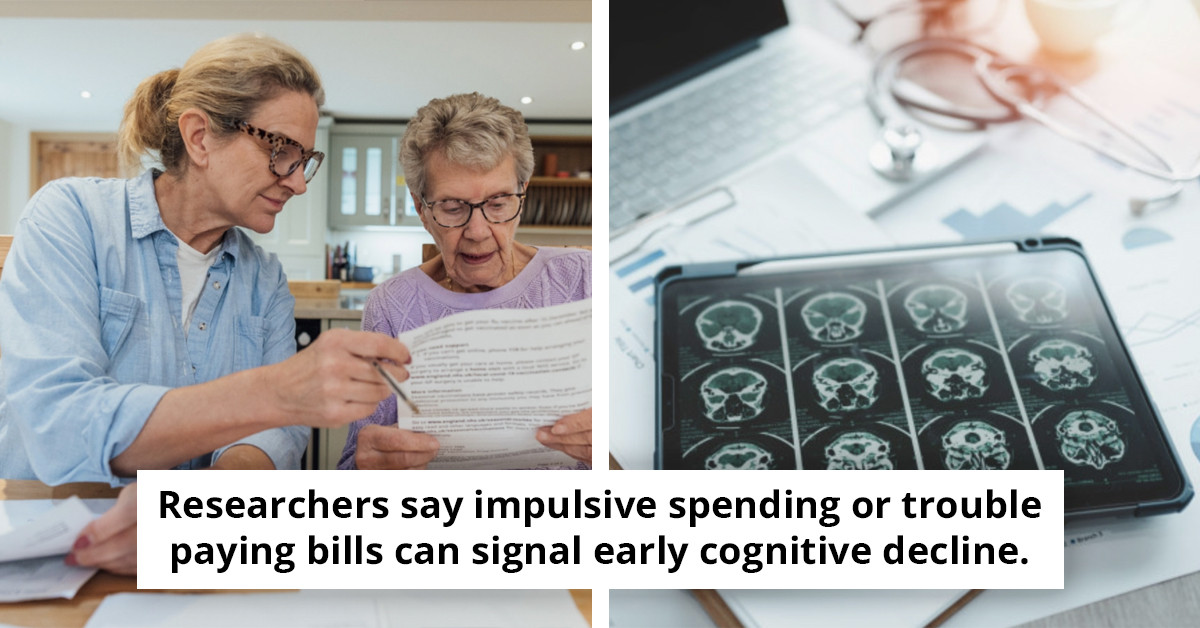

New research reveals that early indicators of dementia could be reflected in your banking activity.

New research links unusual banking activity to early signs of dementia, raising critical questions about how our financial behaviors may serve as red flags for cognitive decline.

It started with something that should have been boring: monthly bills, credit card statements, and the kind of “I’ll handle it later” behavior that never feels urgent until it is.

New research is now pointing to a pattern families can’t ignore. In the years before a dementia diagnosis, people often show early financial trouble, like sliding credit scores and more missed payments, while their day-to-day decision-making gets shakier. And once those numbers start drifting, it creates a messy situation for everyone around them, especially when impulsive purchases and trouble managing money show up at the same time.

For many households, the first warning is not a memory lapse, it’s a bank alert.

Rising Alzheimer’s Cases Among Older Americans

In the United States, it is estimated that approximately 6.5 million people aged 65 and older are living with Alzheimer’s, and this number is projected to rise significantly in the coming decades. Researchers have identified specific behavioral changes, such as impulsive purchases or difficulty managing monthly bills, that may signal early cognitive issues.

These financial anomalies can serve as crucial indicators, prompting families and caregivers to seek evaluations and interventions sooner rather than later. By recognizing these patterns, we can not only enhance awareness but also potentially improve outcomes for individuals at risk of dementia.

That’s when the “impulsive purchases” and “can’t manage monthly bills” stories start sounding less like random bad weeks and more like a pattern in the statements.</p>

Dementia's Impact on Financial Behaviors: Key Symptoms

Alzheimer’s disease and other forms of dementia are often characterized by a range of symptoms, including forgetfulness, confusion, and difficulty with communication. However, there are additional, less frequently discussed symptoms that can manifest in financial behaviors.

These may include impulsive spending, difficulty managing bills, and a general decline in financial decision-making skills, which can have significant repercussions for individuals and their families. A team of researchers from the New York Federal Reserve conducted an extensive analysis utilizing data from U.S.

Financial Decline Precedes Dementia Diagnosis: Key Indicators

Their findings revealed a concerning trend: in the five years leading up to a formal dementia diagnosis, individuals typically experience a decline in their average credit scores, coupled with an increase in payment delinquencies. This decline in financial health serves as a critical indicator of cognitive decline, suggesting that financial management may be one of the first areas to be affected by dementia.

In their published findings, the researchers noted, “The harmful financial effects of undiagnosed memory disorders exacerbate the already substantial financial pressure households face upon diagnosis.” This statement highlights the dual burden that families must bear when a loved one is diagnosed with dementia, as they not only grapple with the emotional toll of the disease but also face significant financial challenges. The study further elaborated on the various ways early-stage Alzheimer’s disease and related disorders can impact an individual’s financial behavior.

The complicated part is how credit scores drift quietly, while payment delinquencies pile up like they’re keeping score for something bigger.</p>

Cognitive Decline: Financial Challenges and Early Warning Signs

They noted that cognitive decline could lead to difficulties in opening new accounts, accumulating debt, managing credit utilization, and maintaining a diverse credit mix. These financial challenges can compound the stress experienced by families, making it imperative to identify early warning signs.

Marcey Tidwell, who experienced the effects of dementia firsthand with his mother’s diagnosis in 2020, shared his personal insights regarding the financial implications of cognitive decline. Tidwell recounted how his mother, who had previously been meticulous in managing her bills, began to exhibit concerning changes in her financial behavior around 2015.

After the Supreme Court’s 6-3 decision, Trump unveiled a major new global tariff, sparking debate over judicial integrity.

Signs of Financial Distress in Her Behavior

He observed that her once-organized records of checks and deposits became chaotic, with numerous corrections and obsessive re-calculations. This shift in behavior was a red flag that something was amiss.

Tidwell also noted that his mother began withdrawing large sums of money from her savings account, far exceeding what she needed for everyday expenses like groceries. This kind of financial recklessness is often indicative of cognitive decline, as individuals may struggle to make sound financial decisions or may not fully grasp the implications of their spending habits.

Even the line about financial pressure hitting families harder lands differently once you realize it’s happening before the formal diagnosis ever shows up.</p>

Financial Behaviors as Indicators of Cognitive Decline

In a related study conducted by researchers from the University of Nottingham and the Lloyds Banking Group, researchers found that everyday financial behaviors could serve as early indicators of cognitive decline. This statement emphasizes the potential for financial institutions to play a pivotal role in identifying at-risk individuals through their banking behaviors.

By leveraging anonymized banking data, financial institutions can develop strategies to protect vulnerable individuals from the adverse effects of cognitive decline. This approach not only serves to safeguard the financial well-being of individuals but also provides a framework for early intervention that could lead to improved outcomes for those diagnosed with dementia.

Importance of Early Detection in Dementia Management

While there is currently no cure for dementia, early detection remains crucial for managing the disease and its associated challenges. The hope is that studies like these will pave the way for more effective screening and detection methods, allowing families to address cognitive decline before it leads to irreversible financial consequences.

A 2020 study from the Johns Hopkins Bloomberg School of Public Health further supports this notion, emphasizing the importance of early screening and detection in protecting patients and their families from financial distress. The lead author of the Johns Hopkins study stated, “Earlier screening and detection, combined with information about the risk of irreversible financial events, like foreclosure and repossession, are important to protect the financial well-being of the patient and their families.” This highlights the critical need for healthcare providers to collaborate with financial institutions to create a comprehensive approach to managing the financial aspects of dementia care.

So when you see the credit score drop and the delinquencies rise in that five-year window, it’s not just “money problems,” it’s a possible early warning sign.</p>

Cognitive Health and Financial Management: A Growing Concern

The intersection of cognitive health and financial management is an area that warrants further exploration.

Empowering Seniors Through Financial Education and Support

By educating individuals about sound financial practices and encouraging them to seek assistance when needed, we can empower older adults to maintain control over their finances for as long as possible. In conclusion, the findings from recent studies underscore the critical importance of recognizing the financial behaviors that may signal early cognitive decline.

By understanding the connection between financial management and dementia, we can better equip families and individuals to navigate the complexities of this disease. As we continue to explore the implications of these findings, it is essential to foster collaboration between healthcare providers, financial institutions, and families to create a supportive framework for those affected by dementia.

Early Detection: Enhancing Lives and Easing Financial Strain

Through early detection and intervention, we can not only improve the quality of life for individuals living with dementia but also alleviate the financial burdens faced by their families. The journey towards understanding and addressing the financial aspects of cognitive decline is just beginning, but it holds the promise of creating a more informed and compassionate approach to dementia care.

This multifaceted issue requires ongoing research, awareness, and collaboration to ensure that those affected by dementia receive the support they need to navigate the challenges ahead. By remaining vigilant and proactive, we can work towards a future where cognitive decline is met with understanding, empathy, and effective solutions that prioritize the well-being of individuals and their families.

The bank notifications might be the loudest clue, long before anyone has the words for what’s changing.

For more executive-power drama, see how the Supreme Court’s 6-3 ruling hit Trump’s tariff authority.